-

Products

- Local Securities

- China Connect

- Grade Based Margin

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- Smart Minor (Joint) Account

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Weekly Specials

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

Shuanghuan Driveline (002472.CH) - Pursues Long-term Growth with New Energy and Robotics Business

Friday, November 8, 2024  5215

5215

Shuanghuan Driveline

| Recommendation | Neutral |

| Price on Recommendation Date | $29.360 |

| Target Price | $32.100 |

Weekly Special - 1361 361 DEGREES

Company profile: Domestic Leader in Automobile Gears

Shuanghuan Driveline specializes in the manufacturing of gear transmission products, with the gear business accounting for about 80% of the Company`s total business. The Company has gradually shifted from traditional gear products to high-precision gears and parts. Its main products span gear products (gears for passenger vehicles, commercial vehicles, engineering machinery, motorcycles and electric tools), reducers and other products, which are mainly applied in the electric drive systems, gearboxes and axles of vehicles, as well as electric tools, rail transit, wind power, industrial robots and other sectors. The Company operates five production bases in Zhejiang, Jiangsu, Chongqing, Dalian and other places.

Founded in 1980, the Company has over 40 years of professional production and manufacturing experience. Relying on such experience, the Company has established close collaborative relationships with numerous customers at home and abroad, connected to the supply chain systems of leading enterprises in various segmentations, and formed a customer base consisting of various industry giants.

In terms of passenger vehicles, the Company has connected with a number of leading enterprises in the automotive industrial chain, including OEMs and transmission parts suppliers, such as world-leading electric vehicle manufacturers, Toyota, Volkswagen, BYD, GAC, GM, Ford, NIO, ZF, Nidec, Schaeffler, Inovance and BorgWarner. The Company boasts a market share of over 70% in terms of gears for domestic high-power new energy vehicles. In terms of commercial vehicles, the Company has established cooperative relationships with ZF, Cummins, Eaton, Yuchai and other core parts companies over the years. In terms of engineering machinery, the Company boasts such representative customers as Caterpillar and John Deere.

Investment Summary

Rapid Revenue Growth

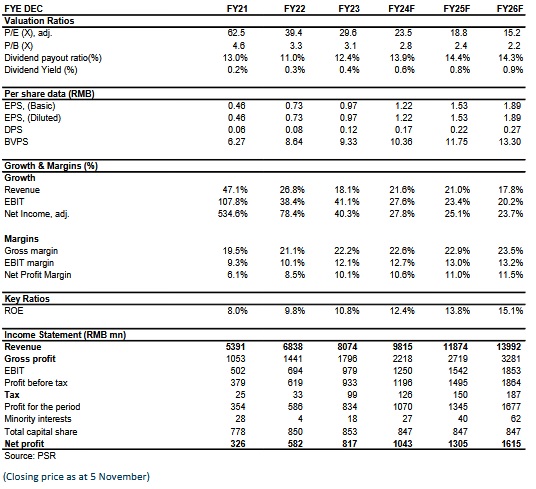

According to its 2024H semi report released, the Company reported an revenue of RMB 4.322 billion, up 17.3% yoy; the net profit attributable to the parent company stood at RMB 473 million, up 28.3% yoy; and the net profit attributable to the parent company excluding non-recurring items was RMB 453 million, up 32.85% yoy. The gross profit margin has increased from 22.24% in 2023 to 22.75% in 2024H1, indicating a continuous improvement in profitability.

On a closer look at the segment revenue, the Company saw steady growth in gears for automatic gearboxes of Intelligent execution mechanism and new energy vehicles. In 2024H1, the Company recorded a revenue of RMB 2.36 billion, RMB 0.46 billion, RMB 0.32 billion, RMB 0.26 billion and RMB0.28 billion for gears in passenger vehicles (up 28.5% yoy), commercial vehicles (up 3.8% yoy), engineering machinery (down 8.3% yoy), reducers (down 18.5% yoy) and Intelligent execution mechanism (up 82.2% yoy), respectively. The revenue from gears for power tools and motorcycles went up by 0.2% and 14.5% to RMB 0.07 billion and RMB0.05 billion, respectively. The gear business generated 75% of the Company`s revenue. In addition, revenue from steel sales increased by 10% yoy to RMB0.5313 billion, accounting for 12.3% of the total revenue.

In terms of gross margin, the gross margin of gears for passenger vehicles, commercial vehicles and engineering machinery stood at 23.4%, 26.25% and 28.9%, respectively, up 3.1pcts, 1.4pcts and 5.1pcts yoy. According to CAAM, in 2024H1 domestic passenger vehicles reported a production volume of 11,886 thousand units and a sales volume of 11,979 thousand units, up 5.4% and 6.3% yoy, respectively; commercial vehicles reported a production volume of 2,005 thousand units and a sales volume of 2,068 thousand units, up 2% and 4.9% yoy, respectively; new energy vehicles reported a production volume of 4,929 thousand units and a sales volume of 4,944 thousand units, up 30.1% and 32% yoy, respectively. With advantages in customer structure, technology and production capacity, the Company significantly outperformed its peers in terms of growth in passenger vehicles and new energy vehicles.

As for expense ratio, the Company`s sales, administrative, R&D and financial expense ratios were 0.949% (up 0.003 ppts yoy), 3.504% (down 0.445ppts yoy), 4.755% (up 0.235 ppts yoy) and 0.387% (up 0.091 ppts yoy), which were attributable to its ongoing measures for cost reduction and efficiency improvement as well as economies of scale. In the years to come, the Company will continue efforts to replace human labour with machines, including intelligent manufacturing systems and big data systems, so as to reduce costs and improve efficiency.

The third quarter performance report for 2024 released by the Company shows that the revenue reached RMB 2.42 billion yuan (up 10.7% yoy), net profit attributable to shareholders arrive RMB 265 million yuan (up 20% yoy), and gross profit margin came to 23.96%,(up 2.26 ppts). The profitability continues to strengthen.

In terms of gears for new energy vehicles, which enjoy high market attention, the Company reached a production capacity of five million units of transmission gear shafts for new energy vehicles at the end of 2023. The capacity utilization rate was high. Moreover, in 2023 the Company decided to establish a production base for gear transmission parts for new energy vehicles in Hungary. The construction will begin in 2024, and the Company will gradually release capacity based on existing orders and its production capacity in 2024 and 2025. In 2024H1, the Company recorded an overseas sales revenue of about RMB 0.62 billion, accounting for 14.3% (0.6ppts higher than 2023) of the total revenue, showing considerable room for improvement. As far as we are concerned, accelerated global capacity will lay cornerstone for the Company`s global expansion.

Seeking Further Expansion and Building a Diversified Product System

Considering the dynamics of the automotive industry as well as the future development trends and competition of the gear industry, the Company has established the concentric diversification development strategy. Specifically, the Company focuses on high-precision gear transmission, seizes the opportunities brought by the booming new energy vehicle market and shift from manual gearboxes to automatic gearboxes and new energy transmission systems of commercial vehicles, and vigorously expands business in such areas as robot joints and people`s livelihood.

First, in terms of gears for Intelligent execution mechanism, in 2023 the Company relied on its holding subsidiary Huanqu Technology, the robust design capabilities of its sub-subsidiary Santohno Intelligent Transmission Co., Ltd. and the operation and manufacturing capabilities of its parent company to actively invest in the R&D of injection molding, related composite material gears and small assemblies. It successively increased its market share in smart home, vehicle-mounted components and other fields, especially in the sweeper industry, which is expected to contribute to the Company`s stable and sustained performance growth in the future.

Second, in terms of robotic reducer, the Company`s subsidiary Fine-Motion Tech has, relying on its R&D and batch delivery capabilities in precision robotic reducers, continuously increased its market share in the domestic RV reducer market. Moreover, it has successfully supplied harmonic reducers.

Investment Thesis

Shuanghuan Driveline is a pacesetter in the domestic automotive gear industry and robotic RV reducer industry. By leveraging its advantages in capacity, management, R&D and customer base, the Company has seized the opportunities for upgrading brought by gear outsourcing and high industry barriers as a result of the booming new energy vehicle industry. Looking forward, the Company is expected to continuously benefit from the boom of new energy passenger vehicles, expansion of the industrial chains of automatic gearboxes of commercial vehicles, and rapid development of robotic reducers and gears for daily use.

As for valuation, we expected diluted EPS of the Company to RMB1.22/1.53/1.89 of 2024/2025/2026. And we accordingly gave the target price to RMB32.1, respectively 26.3/21/17x P/E for 2024/2025/2026. "Neutral" rating. (Closing price as at 5 November)

Risk

Progress of new production line is below expectations

Electric vehicle sales fall short of expectations

Macroeconomic downturn affects product demand

Sharply rising raw material prices or sharply falling product prices

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion 新闻稿 |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

新闻稿

![]()

![]()

![]()

![]()