-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

章晶小姐 (Zhang Jing)

高級分析師

高級分析師

本科畢業於同濟大學工科,碩士畢業於華東師範大學金融貿系。現為輝立証券持牌高級分析師,主要負責汽車及航空板塊的研究,曾獲得《華爾街日報》亞洲區2012年度汽車及零部件最佳分析師第二名,擅長將行業前景與上市公司結合分析。

Bachelor Degree in Tongji University of Engineering; Master Degree in East China Normal University of finance. Currently cover automobile and air sectors. Having worked in research for years and is good at combining analysis for the companies with industry prospects.

| Phone: | 86 21 51699400-103 | Email: | zhangjing@phillip.com.cn | |

HASCO (600741.CH) - Seize the Upgrade Trend to Enhance the Development of Emerging Businesses

Monday, December 9, 2019  5903

5903

HASCO

| Recommendation | Hold |

| Price on Recommendation Date | $25.040 |

| Target Price | $26.000 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

Decline in Net Income Narrows in Q3

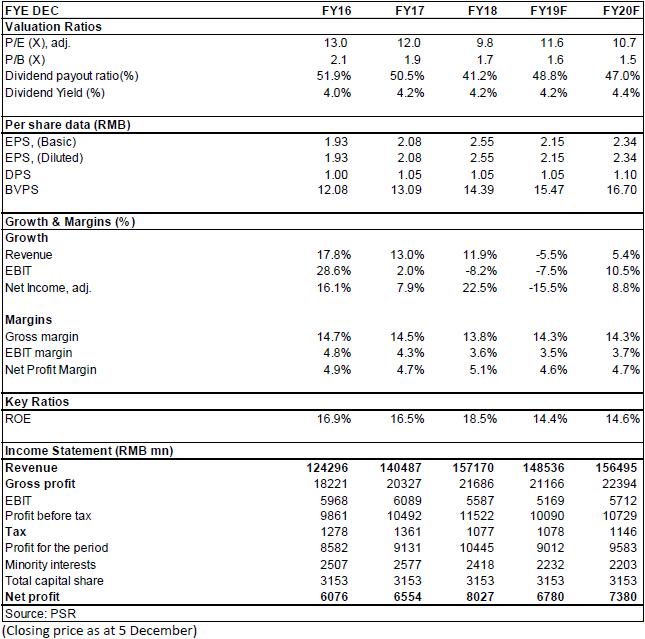

In the first three quarters of 2019, HASCO recorded an accumulative revenue of RMB105,596 million, down by 11.11% yoy, and a net profit attributable to the parent company of RMB4,927 million, down by 22.58% yoy. Excluding the one-time investment income from the acquisition of Koito Automotive Lamp Co., Ltd. in the same period last year, the net profit attributable to shareholders deducting non-recurring losses and gains dropped by 13.90% yoy to RMB4.18 billion in the first three quarters.In Q3, the Company recorded a revenue of RMB35,033 million, down by 5.75% yoy, a net profit attributable to the parent company of RMB1,563 million, almost unchanged and slightly down by 1.7% yoy, and a corresponding EPS of RMB0.4956. The decline in revenue and net income narrowed sharply in Q3.

Better Structure, and the Gross Margin Remains Stable against the Trend

SAIC Motor, the Company's largest customer, saw its output drop by 16.0% in the first three quarters. Driven by the adjustment of customer structure (increased proportion of SAIC Volkswagen) and its overseas business (Yanfeng Global Automotive Interiors), the revenue of HASCO declined less than its major customers, basically staying in line with the industry. In terms of the business composition in Q3, the Company recorded a revenue of interiors and exteriors of RMB2.53 billion (-3.1%), the same of functional parts of RMB7.1 billion (-6.2%), metal moulding and moulds, RMB2.7 billion (-8.8%), and electrical and electronic parts, RMB1.06 billion (+2%), with the net profit contributing RMB780 million (+5.4%), RMB510 million (-21.5), RMB90 million (-18.2%) and RMB70 million (-22%), respectively.

The prices of major raw materials also fell, with a gross margin of 14.5% in the first three quarters, up by 0.7 ppts yoy. In Q3, the Company recorded a gross margin of 14.2%, down by 0.8 ppts qoq, mainly affected by the National Day holiday, production line maintenance and the switching of National Standard VI products of some customers.

Strengthen Cost Control, and Increase R&D Input to Enhance Competitiveness

In the first three quarters, the Company recorded a sales cost ratio of 1.37%, down by 0.07 ppts yoy, a management cost ratio of 5.6%, down by 0.06 ppts yoy, and an R&D cost ratio of 3.63%, up by 1.0 ppt yoy. The decline in the management cost ratio and sales cost ratio reflects the Company's continued cost reduction. The increase in the R&D cost ratio reflects that the Company continued to strengthen R&D efforts in the downturn stage of the industry to ensure its long-term competitiveness.

Operating Cash Flow is Significantly Improved, and Operation Efficiency is Enhanced

Thanks to a narrower decline in the automotive market, better payment collection from whole vehicle manufacturers and the Company's control over costs, the Company's cash flow improved significantly in the first three quarters, with a net flow of RMB1.09 billion. The Company recorded a net cash flow from operating activities of RMB6,625 million, up by 49.9% yoy. And the inventory decreased to RMB9.54 billion from RMB11.41 billion at the beginning of the period, with improved operation efficiency.

Seize the Upgrade Trend to Enhance the Development of Emerging Businesses

Backed by the powerful SAIC Motor, HASCO enjoys obvious competitive strengths in customer, R&D, network layout and capital, and has begun to make achievements in the "electric, networked, intelligent and shared" development of the automotive industry. Its subsidiary Yanfeng Global Automotive Interiors has been designated as the global fixed supplier for the full set of interiors of BMW X5, Mercedes-Benz 206 and other models. Huayu Vision and Bosch Huayu have been designated as the fixed suppliers for the car lamps of GAC Toyota and steering systems of GAC Honda, respectively. And its subsidiaries have been designated as the fixed suppliers of automotive moulds, seats and exteriors products for the battery boxes, assembly parts, side and rear cover moulds, seats and seat sets and bumpers of domestic models of Tesla Shanghai.

In terms of emerging businesses such as intelligent interconnection and electrification of automobiles, the Company has realized the batch supply of its 24GHz rearward millimetre-wave radar to SAIC passenger vehicles, SAIC Maxus and other customers, and its 77GHz frontward millimetre-wave radar has become the first product to pass the test of national laws and regulations and the Company has realized its batch supply to King Long Bus. The Company has also been designated as the fixed supplier of electric air conditioning compressors, electric steering machines and battery trays for new energy vehicles of SAIC Volkswagen MEB, MQB and SAIC-GM BEV3, as well as the fixed supplier of the 48V second-generation hybrid cooling starter generators (48ViBSG) for BMW Brilliance 3 series, 5 series, X3 and X5.

Investment Thesis

In our opinion, in the context of intellectualization/new energy and consumption upgrading, the Company's products are expected to benefit from the rising trend of price and quantity of high value-added products in the future.As analyzed above, we revised EPS expectation of the Company to RMB 2.15 and 2.34 of 2019/2020. And we accordingly gave the target price to 26, respectively 12.1/11.1x P/E for 2019/2020. "Hold" rating. (Closing price as at 5 December)

Financials

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()