-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

China Resource Power (836.HK) - Review on Recent Price Correction in the Power Industry

Wednesday, October 20, 2021  2224

2224

China Resource Power(836)

| Recommendation | Buy |

| Price on Recommendation Date | $18.420 |

| Target Price | $33.400 |

Weekly Special - 3306 JNBY Design Limited

Analysis on Recent Price Correction in the Power Industry:

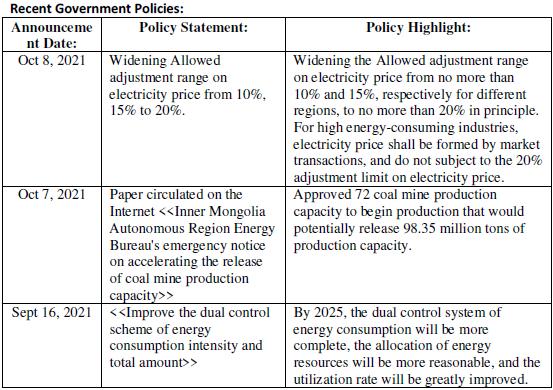

On the evening of October 7, a letter was circulated on the Internet regarding the approval of additional coal mine production capacity in 72 sites in Inner Mongolia. On October 8, the power and coal industries record an approximately 5% - 15% share price correction on a single-day. We view the market correction is due to the concerns with potential increase on coal supply driving coal prices to fall that ultimately affect the pace of electricity price increase. Our take on the news is increase supply of coal is positive for CRP, the increase on thermal coal prices since August has reached about 67%, much higher than the upper adjustment limit on electricity price of 10%/15% (even at the latest revision of 20%). We view increase on coal-supply is positive for CRP. On October 8th, the State Council states the adjustment allowed for electricity prices was raised from about 10%/15% to 20%.

Looking at the longer-term, we maintain the price target of $33.4 HKD for CRP with positive prospects; 1). Accelerated transition to new energy power generation during the 14th-Five Year Plan period and 2). Possibility of A-share fund-raising.

Risk factors:

1. Slowdown on power generation growth.

Increase supply of coal would relieve pressure on coal-fired power generation.

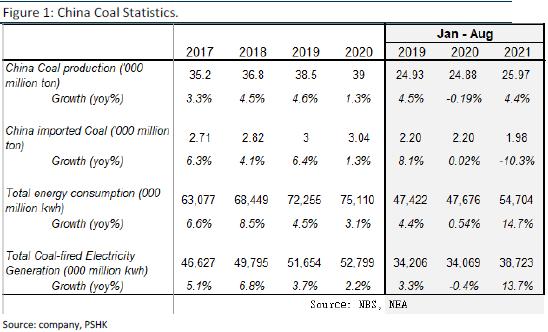

On the evening of October 7, a paper circulated on the Internet named "emergency notice from the Energy Administration of Inner Mongolia Autonomous Region on Accelerating the Release of Part of Coal Mine Production Capacity". The primary takeaway from this paper is 72 coal mines have been approved for additional production that will release about 98.35 million tons of production capacity, accounted for approximately 2.5% of the 3.9 billion tons of raw coal output in China in 2020. Thermal power generation from January to August 2021 increased by 13.7%, however the growth on coal supply is limited. We view thermal power companies are expected to a). Reduce coal prices and operating losses for coal-fired capacity, b). Provide sufficient coal supply to ensure utilization hours.

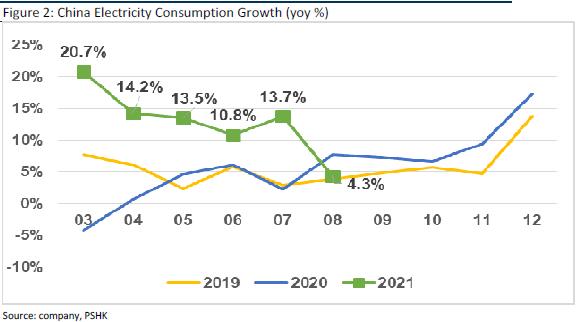

We view the reason for shortage on coal is due to a). Strong demand for electricity consumption. From January to August in 2021, total electricity consumption in China increased by 14.7%/15.4% compared with the same period in 2020/2019. The increase on electricity consumption is at 13.7% that outpace the production increase on coal in China at 4.4%.

Allowed Price Adjustment on Electricity Price widen to 20%, while Energy-Intensive Industries are not subject to the Limit.

On October 8, the executive meeting of the State Council made it clear that "on the premise of maintaining stable electricity prices for residents, agriculture, and public welfare undertakings, the allowed price adjustment on electricity prices shall not exceed 10% and 15%, respectively. In principle, they shall not exceed 20%. For high energy-consuming industries, electricity price are not subject to the 20% adjustment limit. "I view that would relieve the pressure of rising coal-price into the input cost.

Power Consumption Growth Expected to Slow Down in the Coming Months.

According to the Barometer of Completion of Energy Consumption Dual Control Targets in Various Regions in the first Half of 2021 published by the National Development and Reform Commission on August 17 2021, the energy intensity in 9 provinces in the first half of the year did not fall but increased and being issued a first-level warning. Compared with the barometer of the completion of the dual control targets for energy consumption in the first three quarters of 2020, we view the pressure on power curtailment and emission reduction is heavy. It will lead to a reduction on demand for coal-fired generation. We view electricity consumption growth deceleration would relieve pressure on rising coal price and thus improving the operation of CPR.

Risk factors

1) The illness is not controlled as expected

2) Coal prices continue to rise sharply.

3) The scale of new energy installed capacity is less than expected.

4) The price of photovoltaic/wind power equipment has risen more than expected.

5) The subsidy collection rate is slower than expected.

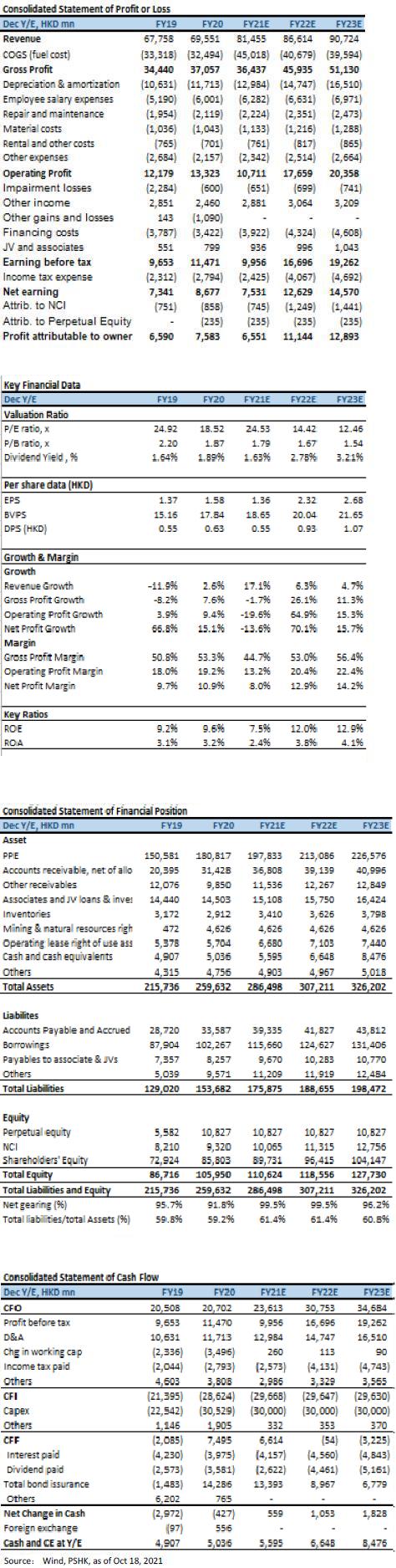

Financial Forecast:

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()