-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Topsports INTL. (6110.HK) - Profit in FY21 was in line with expectations, gradually recovered after the Xinjiang cotton incident

Thursday, June 17, 2021  6855

6855

Topsports INTL.(6110)

| Recommendation | BUY |

| Price on Recommendation Date | $12.020 |

| Target Price | $15.340 |

Weekly Special - 3306 JNBY Design Limited

Investment summary

Profits in FY21 are in line with expectations, and costs are under controlled

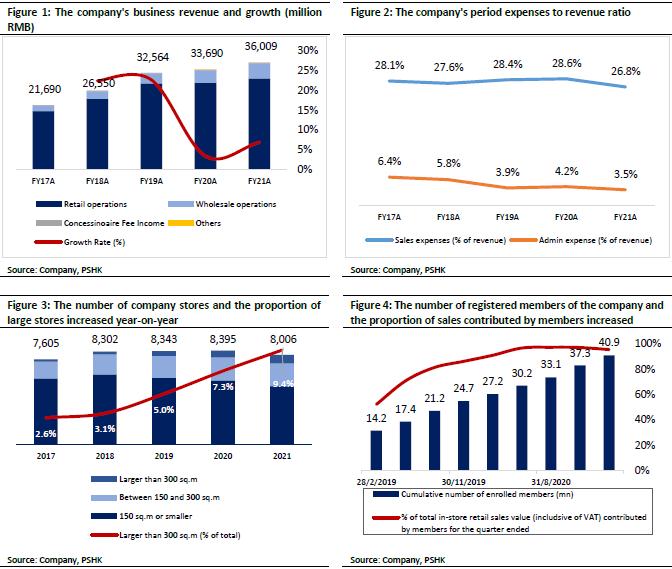

Topsports INT`L announced on May 24 the company's annual results for the year ended February 28, 2021. The company's annual revenue was approximately CNY 36.01 billion, an increase of 6.9% Yoy (2020: CNY 33.69 billion), which was slightly lower than our previous expectation (previous expectation: CNY 37.37 billion), it was approximately 3.6% lower. The company's cost control during the period was adequate, and its OPM improved by 1.3 pcts Yoy, offsetting the slower revenue growth. The adjusted net profit for the year was CNY 2.77 billion, an increase of 16.4%, which was in line with our expectations (previously expected: CNY: 27.67) Billion). The company proposes to distribute 12 cents per share for the final period. Together with the interim dividend, the dividend payout ratio is approximately 54% (excluding special dividends). The annual dividend (including one special dividend) totals 64 cents per share.

Revenue recorded SD growth, strategically increasing the proportion of wholesale business

Topsports` annual revenue was 36.01 billion yuan, an increase of 6.9% Yoy. The company's revenue growth in 1H and 2H was -7% and +21%, respectively. Compared with the 2H19, revenue in 2H21 also increased with DD growth. In terms of business segment, the company's retail business revenue was CNY 30.73 billion, an increase of 5.4%, the wholesale business was CNY 4.95 billion, a Yoy increase of 17.3%, and joint operating expenses were CNY 240 million, a Yoy decrease of 9.8%. E-sports revenue was CNY 80 million yuan, an increase of 168.1%. During the period, the company's retail/wholesale/concessionaire fee income/e-sports revenue accounted for 85.3%/13.8%/0.7%/0.2%, and the wholesale business accounted for an increase of 1.3pcts, mainly due to the company's strategic increase in the proportion of approved business during the year. If divided by brand, the company's main source of revenue is the main brand, with revenue reaching CNY 31.42 billion, an increase of 6.6%, accounting for 87.3% of the revenue; while the revenue of other brands was CNY 4.27 billion, an increase of 9.3%.

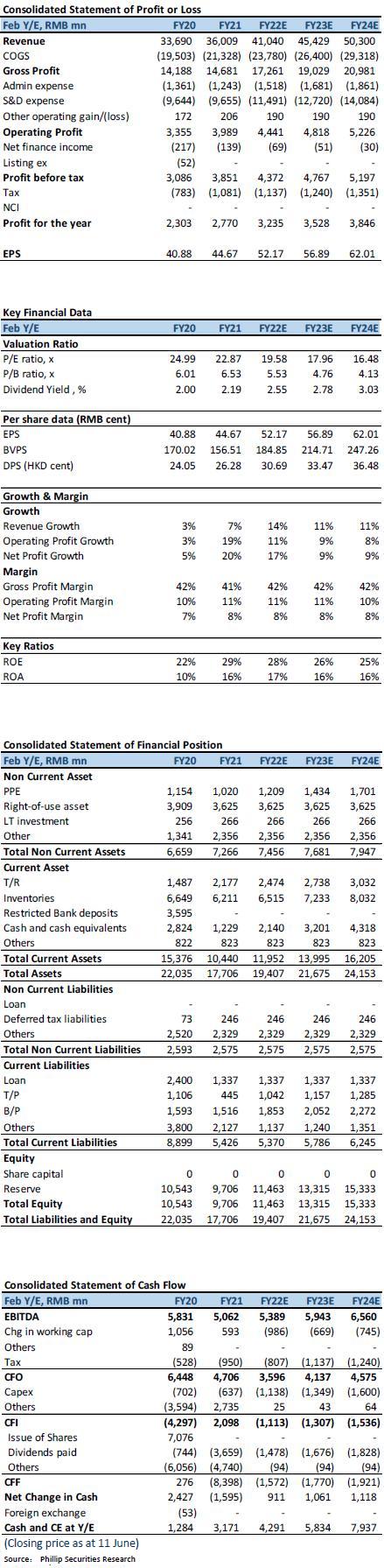

In terms of profitability, the company's GPM decreased by about 1.3 pcts to 40.8% compared with last year, slightly lower than expected (previously expected: 41.6%), mainly due to the company's increased sales discounts to customers during the epidemic. The annual gross profit was CNY 146.8million. The company's cost control during the period was adequate, and the sales and distribution expense ratio and the administrative expense ratio were 26.8% and 3.5%, respectively, which improved compared to the same period last year (the same period last year: 28.6% and 4.2%). The decrease in sales and distribution expense ratio was mainly due to the decrease in staff costs and leasing costs as a percentage of revenue. In 1H21, due to the epidemic, the company received a certain amount of rent reduction and exemption. In 2H21, it has gradually returned to normal (1H/2H ratio changed Yoy: -1.8 ppts/+0.2 ppts). In terms of administrative expenses, it was mainly due to the one-off listing expenses (CNY 52 million) that were included in the same period last year, and no listing expenses were recorded this year.

Stores continue to be optimized, and the proportion of large stores continues to increase

The company focuses on its own strategy and continues to prioritize and optimize stores. In terms of the number of stores, the company's direct-operated physical stores for the year decreased by 389 Yoy, with net closures of -239/-150 stores in the first and second half of the year, but the gross sales floor area increased by 4.1%. In terms of the size of stores, the proportion of large stores above 300 square meters continued to increase. As of February 28, 2021, the number of large stores above 300 square meters was 750, an increase of 138 Yoy, and the proportion increased by 2.1 ppts to 9.4%. The number of large stores opened in 1H21/2H21 was 37 and 101 respectively; the proportion of stores from 150 square meters to 300 square meters continued to increase; most of the closed stores were small stores below 150 square meters, a Yoy decrease of 540, and the proportion also decreased to 64.8%. The store changes show that the company has continued to optimize channel combing to provide customers with a high-quality offline experience, and store efficiency continues to improve.

Promote online and offline integration

During the epidemic, the company continued to expand its online membership and provided diversified membership activities and services through global consumer reach. As of February 28, 2020, the company's cumulative registered members increased by 3.6 million quarterly to 40.9 million. In-store retail sales contributed by Q1/Q2/Q3/Q4 members accounted for 96.7%/97.3%/97.1%/95.3% of the total. The Topsports sports app has been online for more than a year. As of February 28, the number of users has exceeded 2.7 million to build a user community and increase customer stickiness. In the second half of the fiscal year, an online community "Tao Ker" will be added for members to share here. Exchange experiences and create an online sports lifestyle community. In the future, the company will focus on online and offline integration to achieve seamless interaction with consumers in physical and virtual scenarios, including increasing the coverage of store-based social programs and opening mobile cashier tools.

Follow-up to Xinjiang Cotton Incident

After the incident, the company suffered a greater negative impact on sales in the first three weeks, and it has now begun to gradually recover. Sales in April recorded a positive growth Yoy in 2020, and sales during the May 1st period compared to the same period in 2019 have also returned to positive Growth, the company maintains its annual growth target. In the early stage of the incident, the company paid close attention to the development of the situation and terminal sales performance. Through the dynamic management of goods, discount control and store management, and the support of brand owners, the impact of the incident was reduced.

Valuation and investment advice

The company was affected by the epidemic last year and gradually recovered in the second half of the year. In terms of revenue, it recorded a MSD growth compared with the same period last year, which was lower than our previous expectations. However, the company's cost control during the period was adequate and the profit side was in line with our previous expectation. Affected by the Xinjiang cotton incident, it has a negative impact on the company's sales in the first quarter of this fiscal year, but it has gradually recovered recently. We lowered the company's revenue forecast in FY22 to CNY 41.04 billion (previous forecast: CNY 45.10 billion), raised the company's GPM to 41.9% (previously: 41.4%), and lowered the company's sales expense ratio and administrative expense ratio to 28.0% and 3.7% respectively (previously: 28.5% and 3.8%). The overall profit forecast is revised up by 4.0% to CNY 3.24 billion. Raise the target price to HKD 15.34, corresponding to the FY22E/FY23E P/E ratio of 25.0x/22.9x, and upgrade the rating to BUY.

(Closing price as at 11 June)

Risk

1) The impact of COVID-19 continues 2) The business relies on two major brands 3) The cash level is at a low level due to the dividend policy 4) Major brands are affected by the boycott

Financial

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()