-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

CMGE (302 HK)- Leading IP-based game operator and publisher

Thursday, July 9, 2020  15687

15687

CMGE (302 HK)(302)

| Recommendation | Buy |

| Price on Recommendation Date | $3.490 |

| Target Price | $4.450 |

Weekly Special - 3306 JNBY Design Limited

Investment Summary

Leading IP-based game operator and publisher

CMGE is focusing primarily on IPs relating to well-known cultural products and art works, such as icons or characters from popular animations, novels, and motion pictures, which have a significant fan base, market acceptance and commercial value. According to the prospectus, amongst all Chinese independent mobile game publishers, the company had the largest IP reserve that can be used to develop into IP-based games as of June 30, 2019.

The company is committed to develop oversea businesses

The company's revenue from overseas games in 2018 and 2019 were RMB 10.54 million and RMB 13.34 million, an increase of 26.6% yoy. The company expects to launch a number of games in oversea regions in 2020, including famous IP games such as "Dynasty Warriors: Hegemony"「真 · 三國無雙:霸」. "Dynasty Warriors: Hegemony" is highly anticipated by market players. It ranked first in the TapTap reservation list for three consecutive days at the end of December 2019 and received excellent rating of Android 9.0 and iOS 9.7. Based on the above reason, we believe that the company's overseas revenue and its ratio to total revenue in 2020 will be greatly improved. In addition, the company's commitment to expand its overseas game business can help it to reduce and get rid of the increasingly stringent risks of game approval in the Chinese market.

The company has developed an in house game development segment and is committed to improve its ability to develop games internally

In 2018, the company has acquired Wenmai Hudong and Beijing Softstar, which has provided the company ability to develop games internally. The revenue from game development has increased by 137% and reached RMB 421 million in 2019. It is expected that the company will launch a total of 9 internally developed games in 2020, including the highly anticipated “ Thunder Empire 2”. Hence, we expect that the company’s revenue from game development and the proportion of it to total revenue will increase in 2020. We also believe that through its continuous improvement of internal R&D capabilities, the company can increase its profit margin and obtain more high-quality IPs in the future.

IP based game sector has an advantage within the game sector

One of the major advantages of IP games is that the fans of its own IP can easily be converted into game players, so the marketing and promotion costs of the IP based games are lower than those of non-IP games. Secondly, this group of fans usually have higher loyalty and stickiness, hence, the average life cycle of IP game is longer than non-IP games. According to Analysys, the average life cycle of mobile games is 6-12 months, while the life cycle of CMGE’s IP based games are ranging from 1-4 years. Based on the above reasons, compared with non-IP game companies, IP game companies have the characteristics of more stable revenue and higher liquidity.

Valuation

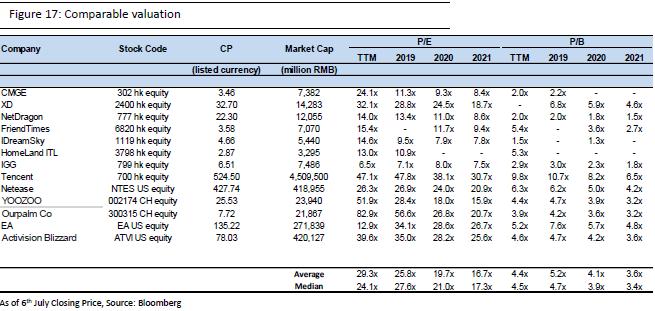

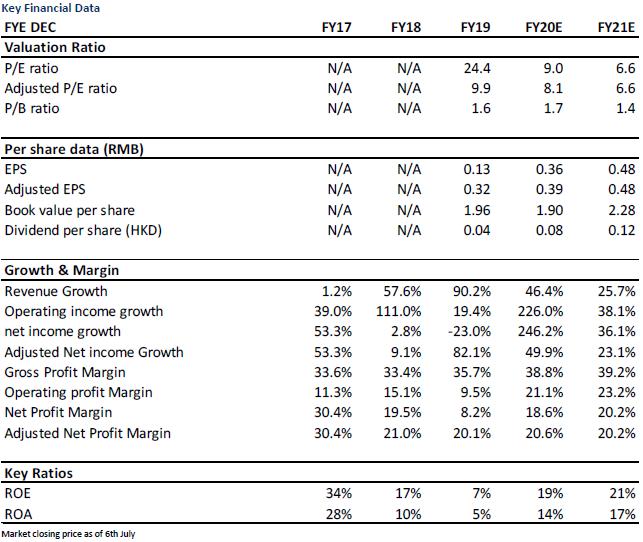

We believe that the company has a huge potential of growth. We forecast the adjusted EPS of the company in 2020E/2021E are 0.39/0.48 RMB (0.43/0.52 HKD). Our target price is 4.45 HKD, which implies a P/E ratio of 10.4x/8.6x on 2020E/2021E adjusted EPS. We initiate with a “BUY” rating. (Market closing price as of 6th July)

Risks

The risks to our target price are 1) failure in licensing IPs and games 2) failure in developing games in-house 3) failure to obtain or maintain all applicable permits and approvals 4) loss or deterioration of our relationship with game developers and publishing channel 5) The revenue generated from games are below expected.

Industry Review and Forecast

The mobile game market is the segment with the most growth potential within the Game industry

Since 2015, China has been the world’s largest market of online games in terms of gross billings. One of the main reasons for the boom of China’s online game market was the intensified demand for entertainment. According to Frost and Sullivan, China’s online game market reached a size of RMB257 billion in 2019, and is expected to reach RMB398 billion in 2024, representing a CAGR of 9.1%. With the advancement of hardware and internet technology, the graphics, content and response speed of online games are being constantly upgraded, the development of online games are more tailored to player preference. Mobile game sector is the main sub-segment in the game sector with its growth higher than other sub-segments (client game sub-segment and web game sub-segment). China’s mobile game market expanded from RMB98 billion in 2016 to RMB181.7 billion in 2019, and is expected to reach RMB316 billion in 2024, representing a CAGR of 11.7%. We believe that with the ongoing development of gaming online broadcast and the e-sport industry, as well as the increase proportion of mobiles in population, the mobile game sub-segment is likely to slowly replace the other sub-segments.

Compared to other forms of entertainment, residents of China spend more on games and this proportion has an upward trend. According to Analysys, China’s expenditure on games accounted for 38.2% of their total entertainment expenditures in 2016, which increased to 39.1% in 2017 and further to 39.4% in 2018. it is expected that expenditure on games will continue to grow in the future. The size of China’s mobile game publishing market was RMB38.8 billion in 2016, which increased to RMB47.3 billion in 2017 and RMB50.8 billion in 2018, and is expected to reach RMB62.8 billion in 2021, representing a CAGR of 10.1%. The growth of China’s mobile game market has attracted an increasing number of mobile game developers. Publishing channels such as Apple’s App Store and application stores for Android system became the major publishing channels of mobile games.

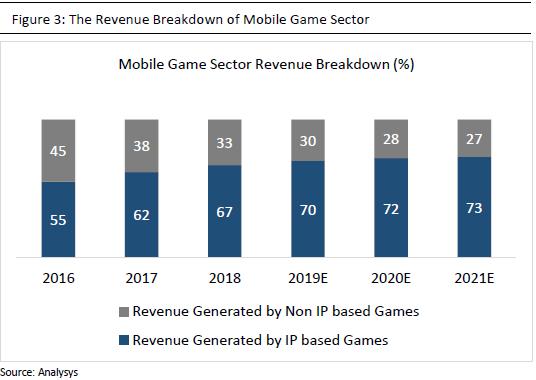

Within the Mobile Game segment, the proportion of revenue from IP-based games is increasing

In 2018, on Apple’s App Store, 71.0% and 61.0% of the top 50 free games and the top 50 grossing games in terms of revenue generation, respectively, were developed based on IPs. In 2018, IP-based mobile games generated revenue of RMB97.2 billion, which is expected to increase to RMB167.9 billion in 2021, representing a CAGR of 20.0%. The chart below illustrates the revenue generated by IP and non-IP based games. With increasing player demand for high-quality games, IP owners will be selective in licensing out their IPs to game developers or publishers that have proven operational capabilities for IP-based games. Therefore, we believe that CMGE will be able to obtain more and more IPs in the future and further expand its business by leveraging on its existing IP reserves and its leading position in the industry.

Company Overview and its Competitive Advantages

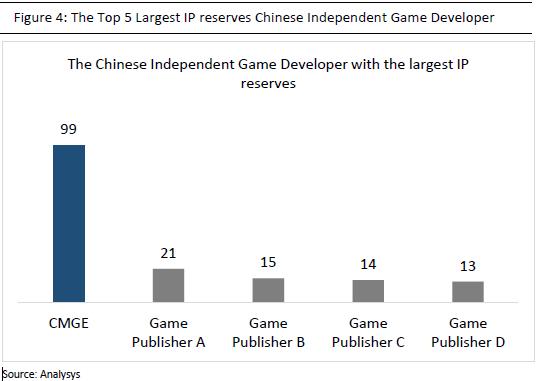

CMGE has one of the largest IP reserve among all Chinese independent mobile game publisher

According to Analysys, among all Chinese mobile game publisher, GMGE has the second largest IP reserve (99 IPs), just behind the market leader Tencent. Among all Chinese independent mobile game publishers, CMGE has the largest IP reserves. As at 31 December 2019, the Group had a vast IP reserve comprising 31 licensed IPs and 68 proprietary IPs. Among these IPs, majority of them are popular animations (ie Naruto and One Piece). These kind of IPs have a huge fan base of the younger generation. Besides that, CMGE has already established a long term partnership with major IP owners across the world (ie SNK and Toei Animation). Therefore, it is likely that the IP reserve of the company will continue to grow in the future.

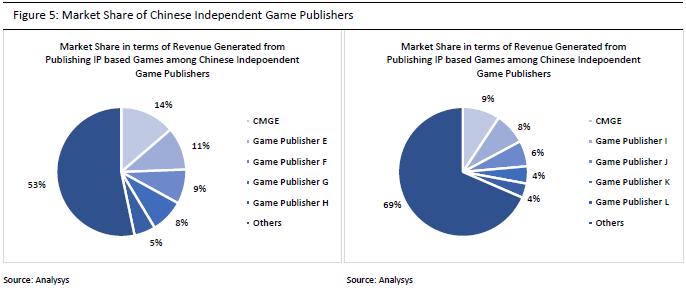

According to Analysys, during the period commencing from January 1, 2015 to June 30, 2019, and amongst all Chinese independent mobile game publishers, CMGE ranked first in terms of the cumulative revenue generated from publishing IP-based games and numbers of IP games Published.

The Company has a diversified, commercially successful and extensive mobile game portfolio

For the period between 1 January 2016 and 31 December 2019, the Group launched 107 games, among which, 73 games are still active as of 31st December, 2019. By leveraging on its large IP reserve, the company is expected to publish 38 new games, including the highly anticipated Xuan Yuan Sword – the Origin (軒轅劍:劍之源) and The New Legend Of The Condor Heroes: Iron Blood and Loyal Heart (新射雕群俠傳:鐵血丹心). The Xuan Yuan Sword – the Origin (軒轅劍:劍之源) was launched in late April, 2020 and with its high influence in the industry, the game achieved 2nd place in the APP Store free APP ranking only 8 hours after launching.

IP based game sector has an advantage within the game sector

One of the major advantages of IP games is that the fans of its own IP can easily be converted into game players, so the marketing and promotion costs of the IP based games are lower than those of non-IP games. Secondly, this group of fans usually have higher loyalty and stickiness, hence, the average life cycle of IP game is longer than non-IP games. According to Analysys, the average life cycle of mobile games is 6-12 months, while the life cycle of CMGE’s IP based games are ranging from 1-4 years. Based on the above reasons, compared with non-IP game companies, IP game companies have the characteristics of more stable revenue and higher liquidity.

The company has developed its in-house game developing team and is committed to improve its ability to develop games internally

In 2018, the company has acquired Wenmai Hudong and Beijing Softstar, which has provided the company ability to develop games internally. The revenue from game development has increased by 137% and reached RMB 421 million in 2019. The World of Legend – Thunder Empire (傳奇世界之雷霆霸業), which is an in house developed game published in late 2018, has been a huge success. It recorded peak gross billing in a single month of over RMB200 million and nearly 1.3 million average MAUs. It is expected that the company will launch a total of 9 internally developed games in 2020, including the highly anticipated “ Thunder Empire 2” (雷霆霸業2). Hence, we believe that the company’s revenue from game development and the proportion of it to total revenue will increase in 2020. We also think that through its continuous improvement of internal R&D capabilities, the company can increase its profit margin and obtain more high-quality IPs in the future.

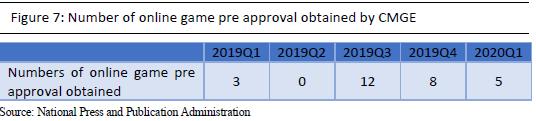

The Group is able to obtain online game pre-approvals for its games

Obtaining pre-approvals from government departments responsible for publication

administration and the National Press and Publication Administration (國家新聞出版署) prior to publishing domestically developed games is extremely important for game publisher. Failing in which could lead to the shutdown of the game publisher or subject the game publisher to fines. The company has obtained pre-approvals for 23 and 5 games in 2019 and first quarter of 2020 respectively. These numbers are even higher than the industry leaders, Tencent and Netease, which have only received pre-approval for 19 games each for the same period. The high number of pre-approvals is likely to help build a strong foundation for the company’s operation in future.

The company is committed to develop oversea businesses

The company's revenue from overseas games in 2018 and 2019 were RMB 10.54 million and RMB 13.34 million, with an increase of 26.6% yoy. The company expects to launch a number of games in oversea regions in 2020, including famous IP games such as "Dynasty Warriors: Hegemony"(真·三國無雙:霸). "Dynasty Warriors: Hegemony" (真·三國無雙:霸) is highly anticipated by market players. It ranked first in the TapTap reservation list for three consecutive days at the end of December 2019 and received excellent ratings of Android 9.0 and iOS 9.7. Apart from that, the company has established a team which is solely responsible for overseas game development. So far, the revenue from overseas games has only contributed 1% of the total revenue. Based on the above mentioned reasons, we are confident that the company's overseas revenue and its proportion to total revenue in 2020 will be greatly improved. In addition, the company's commitment to expand its overseas business can help it to reduce and get rid of the increasingly stringent risks of game approval in the Chinese market.

The Group has a large publishing network for mobile games in China

Through years of operation experience in the mobile game sector, the company has accumulated a huge distribution network in game publishing. The company is able to publish mobile games on all major game platforms across China, including major domestic and international application stores, third-party open platforms, application stores operated by mobile phone manufacturers, and social network platforms. The Group has also entered into exclusive licensing agreements with ByteDance (字節跳動) and Tencent(騰訊). This can allow the company to promote its games to a larger and more diverse user base. In addition, the company has acquired its own publishing platform, namely VClub (勝利俱樂部), in September 2018. For games published this platform, the company collects gross billings directly from payment channels which can help increasing the margin of the company.

CMGE is likely to become a major business partner of ByteDance and grow rapidly from it

Since 2018, ByteDance has entered the online game industry. Although ByteDance has abundant resources, nonetheless, it has entered the online game industry later than the other game giants (such as Tencent and Netease). As a result, the relatively bigger and more popular IPs has been already locked by these game giants. We believe that if ByteDance intends to continue its adventure in the online game sector, it will inevitably have to confront with these game giants in the future. Hence, the chance of ByteDance to cooperate with these game giants is very low. Rather, ByteDance would have to search for cooperation opportunities with the second tier game companies and would have to provide a very attractive offer to attract these companies. We think that what ByteDance is lacking the most right now is the resources of IPs. On the other hand, CMGE is known for its large and popular IP reserve. Further, CMGE has worked with ByteDance in the past and have achieved very impressive results together. As a consequence, we believe that CMGE is one of the obvious working partner choice for ByteDance and CMGE is likely to grow rapidly from the corporation by benefiting from the resources provided by ByteDance.

The recent Chinese policies on preventing the addiction of underage’s players is unlikely to have a huge effect on the company

The Chinese government has previously stated that in order to prevent the underages from indulging in online games and excessive consumption, it will fully implement real-name authentication of games to identify players' real age and will strictly control the game time of the underages. The underages are not allowed to play video games after 10 pm and before 8 am. They can only play a maximum of 90 minutes on weekdays and a maximum of 3 hours during weekend and holidays. Despite the strict policies, we believe that it is unlikely to have a huge effect on the company’s revenue and operation. This is because the company’s pay users are mainly adults ranging from 19-38 years old. Besides that, the company has also stated that they will strictly follow the policies and has already set up the corresponding anti-addiction control system for the underage players.

Active Investment along its Value Chain in recent years

The company has invested in 20 well established game developers (17 direct investments and 3 in the form of convertible bond investments). This allow the company to have a continuous supply of high quality games (including the One Piece – The Voyage (航海王熱血航線), which is expected to be published in 2020 Q4). Further, the company has invested in different IP owners and IP incubating platforms through CPC Fund. This allows the company to maintain close relationships with the IP owners and to obtain high quality IPs in the future. The company is currently holding 25.7% of CPC Fund’s limited partnership interests.

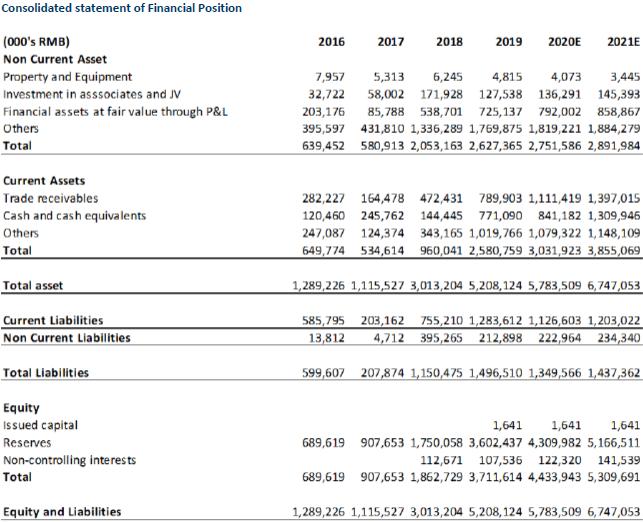

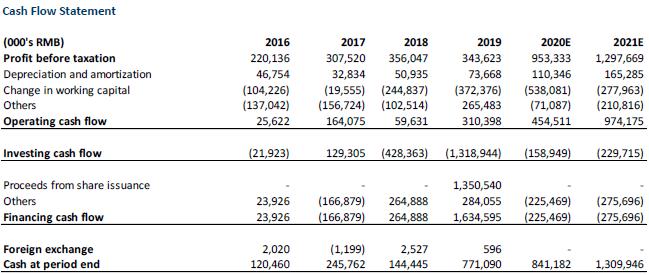

Financial Analysis and Forecast

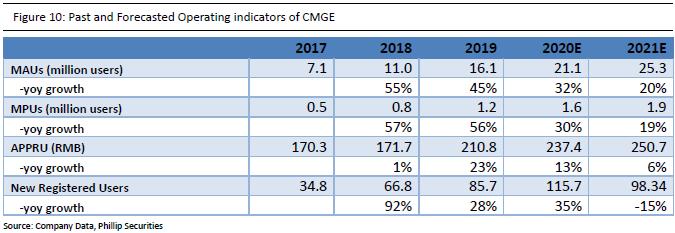

Operating Indicator

We believe that the operating indicators of the company will increase in 2020 and 2021. Firstly, due to the impact of COVID 19 and the quarantine policies in China, the demand for games from the Chinese residents have greatly increase in the first half of 2020. According to App Annie, the amount of mobile games downloads has hugely increase in the three months since the outbreak. Comparing with the number in 2019 Q4, the average weekly mobile games downloads have increased by 30% and reached over 1 billion downloads. Based on this, we believe that the company’s new register users in 2020 will increase by a significant amount and reach 116 million, up by 35% yoy. However, we expect the new register users of 2021 will normalized to pre COVID-19 outbreak level of around 98 million.

Further, we also believe that the month active users (MAUs) and monthlu pay users (MPUs) of the company in the next two years will rise. One of the main reason is that the company is planning to publish 38 new games in 2020, including multiple “masterpiece” such as The Xuan Yuan Sword – the Origin (軒轅劍:劍之源), Dynasty Warriors: Hegemony (真·三國無雙:霸), Legend of Sword and Fairy 7 (仙劍奇俠傳7) and Soul Land (斗羅大陸). These IP games all have a huge fan base with great loyalties. Besides that, the company is expected to launch 4 games with the “Internet giants” such as ByteDance (字節跳動) and Tencent(騰訊). According to the past data, games published alongside with these “internet giants” tend to have a relatively high MAUs. Based on the above points, we forecast that the MAUs for 2020 and 2021 will be 21.1 million and 25.3 million users, up by 32% and 20% respectively. On the other hand, the MPUs for 2020 and 2021 will be 1.56 million and 1.86 million respectively.

Lastly, as the proportion of expenditure on games to total entertainment expenditure and the proportion of IP based mobile games revenue to total revenue of mobile games continue to rise, plus the impact of COVID-19 to mobile game sector, we expect that the average revenue per month per paying user (ARPPU) will grow significantly in the 2020. After that, there will be a normalization of APPRU growth rate in 2021. We forecast that the AAPPU of 2020 and 2021 will be 237RMB and 251RMB in 2020 and 2021 respectively, increased by 13% and 6% respectively.

Revenue

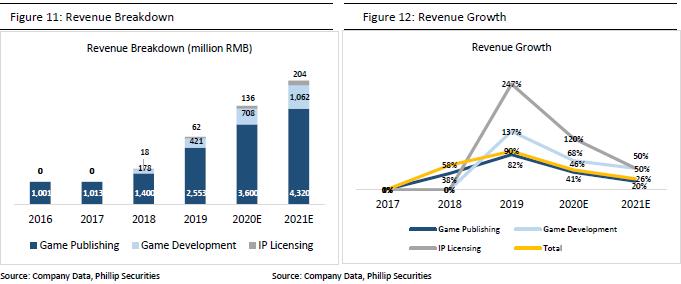

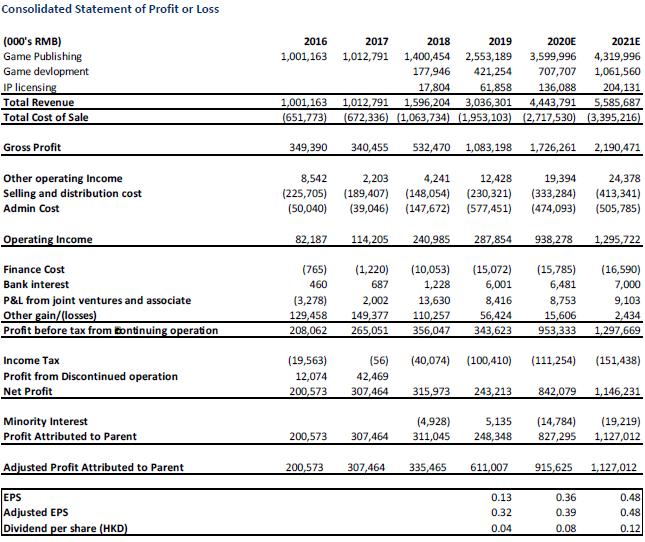

The company’s revenue has increased from RMB 1billion in 2016 to RMB 3.04 billion in 2019, with a CAGR of 45%. We expect that the revenue of the company in 2020 and 2021 will be RMB 4.44 billion and RMB 5.59 billion, implying a CAGR of 36% from 2019-2021. We believe that the revenue growth will be mainly attributed by the rise in both MPUs and APPRU in the next two years. We forecast that the revenue from game publishing of 2020 and 2021 will be RMB 3.60 billion and RMB 4.32 billion, representing a CAGR of 30% from 2019-2021. Although, the proportion of revenue from game publishing will still contribute the most to the total revenue in the next two years. However, we strongly believe that the revenue driven from internal developed game development will become a new driver of revenue in the future. In 2018, the company has acquired Wenmai Hudong and Beijing Softstar, which has provided the company ability to develop games internally. The revenue from game development has increased by 137% and reached RMB 421 million in 2019. We believe that this figure will reached RMB 708 million and RMB 1.06 billion in 2020 and 2021 respectively. In addition, even though we expect the company’s revenue from the licensing of proprietary IP to third parties will have a huge growth in the upcoming years. Nonetheless, it will only contribute an insignificant proportion to the total revenue of the company. We forecast that the revenue from the licensing of proprietary IP to third parties will be RMB 136 million and RMB 204 million.

Gross Profit and Margin

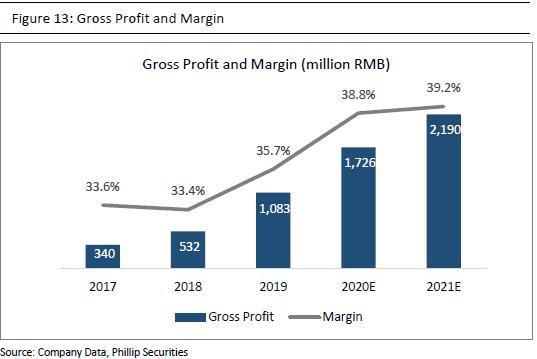

The company’s gross margin of previous few years are relatively stable with a slight upward trend. The gross margin for 2017, 2018 and 2019 were 33.6%, 33.4% and 35.7% respectively. The increase in gross margin in 2019 was mainly attributed by the fact that the company acquired its own publishing platform, namely VClub (勝利俱樂部), in September 2018. For games published through this platform, the company collects gross billings directly from payment channels which helped increasing the gross margin of the company. In addition, ever since 2019 ,the company is committed to internal game development and internal game development tends to have higher gross margin. Since we believe that the company will continuing focusing on internal game development in the foreseeable future, hence, we expect the overall gross margin of the company will also rise in the upcoming years. We forecast that the company gross profit in 2020 and 2021 will be RMB 1.73 billion and RMB 2.19 billion, up by 59.3% and 26.9% yoy, with the corresponding gross margin of 38.8% and 39.2%.

Other Expenses and Operating Profit

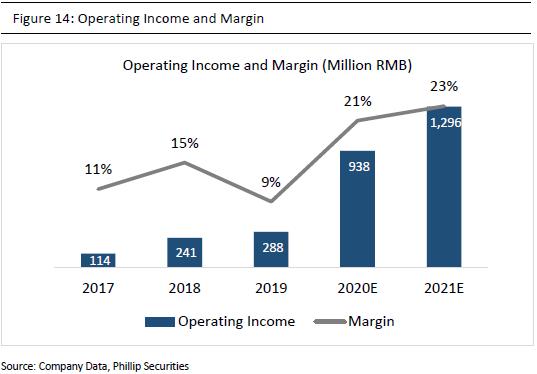

The major reason why marketing expense (the expense with the highest proportion within selling and distribution expense) to revenue ratio has a decreasing trend for the past few years was mainly attributed to the change in marketing strategies to focus on targeted advertising to attract more relevant user traffic with improved cost efficiency. We expect this trend will continue over the next two years. Hence, we expect the overall selling and distribution expense to revenue ratio will also decrease for the next two years. Our forecast of selling and distribution expense to revenue ratio are 7.5% and 7.4% respectively for 2020 and 2021. Further, we expect the equity settled share based expense is likely to decrease hugely in 2020 and 2021. This will drag down the administrative expense/revenue ratio for 2020 and 2021. We forecast that the admin expense/revenue ratio for 2020 and 2021 are 10.7% and 9.1% respectively.

Based on the above reasons, the overall operating income margin is likely to increase in 2020 and 2021. We forecast that the operating income are 938 million and 1.30 billion RMB, with the corresponding operating income margin at 21% and 23%.

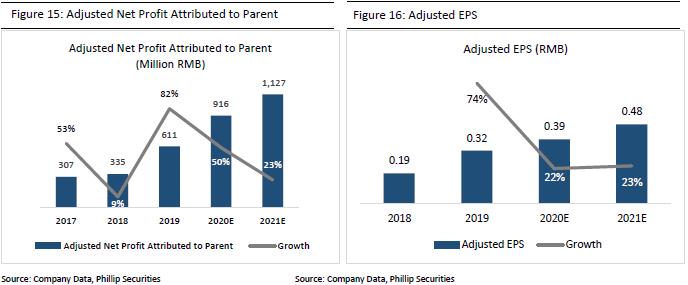

Adjusted Net Profit Attributed to Parent and Adjusted EPS

We believe that comparing with Net profit attributed to parents, adjusted net profit attributed to parent can better reflect the company’s result and performance. This is because the Net profit attributed to parents is after the deduction of the equity-settled share-based expense and listing expenses in 2019, which are one-off non-operating expenses. The adjusted net profit attributed to parent has increased from RMB 200 million in 2016 to RMB 611 million in 2019 with a CAGR of 45% from 2016-2019. We forecast that this figure will reach RMB 916 million and RMB 1.13 billion in 2020 and 2021, with corresponding adjusted EPS as 0.39 RMB and 0.48 RMB.

Valuation

We have set a target price of 4.45 HKD

We believe that the company has a huge potential of growth. We forecast the adjusted EPS of the company in 2020E/2021E are 0.39/0.48 RMB (0.43/0.52 HKD). Our target price is 4.45 HKD, which implies a P/E ratio of 10.4x/8.6x on 2020E/2021E adjusted EPS. We initiate with a “BUY” rating. (Market closing price as of 6th July)

Financial Statements

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()