-

Products

- Local Securities

- China Connect

- Grade Based MarginNEW

- Stock Borrowing & Lending

- IPO

- Stock Options

- Foreign Stocks

- Unit Trust

- Local Futures

- Foreign Futures

- Forex

- Bullion

- Insurance Services

- Bond

- Monthly Investment Plan

- Mortgage

- Other Services

- Surplus Cash Facility

- Phillip Premier

- Latest Insurance Promotion<

- ETF

- Capital Management

- Research

- Market Info

- Education Center

- Phillip Apps

- Customer Service

- About Us

-

Surplus Cash Facility

Research Report

Author

研究部 (Research Team)

輝立証券

輝立証券

| Phone: | (852)22776555 | Email: | research@phillip.com.hk | |

Report Review of July 2021

Wednesday, August 4, 2021  4654

4654

Report Review of July 2021

Weekly Special - 3306 JNBY Design Limited

Sectors:

Air & Automobiles (Zhang Jing),

Consumer & Property Management (Timothy Chong)

TMT (Samuel Sung)

Automobile & Air (ZhangJing)

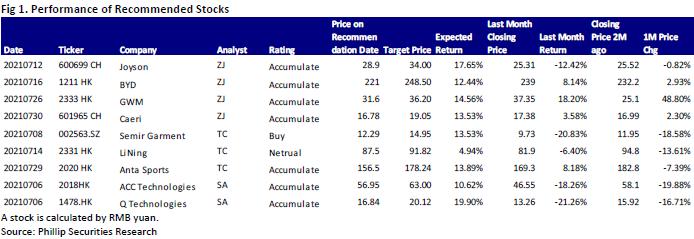

This month I released 4 updated reports of Joyson(600699.CH), GWM (2333.HK), BYD (1211.HK) and Caeri (601965.CH) which got success by their unique Competitive edge. Among them, we highly recommend GWM (2333.HK), BYD (1211.HK).

According to the results report, in the first half of 2021, GWM reported operating revenue of RMB62.16 billion, up by 73.0% Y-o-Y. The net profit attributable to the parent company was RMB3,498 million, up by 205.2% Y-o-Y. In H1, GWM sold 618,200 vehicles accumulatively, up by 56.47% Y-o-Y. The three major technology brands, including Lemon, Tank and Coffee Intelligence, have significantly boosted the Company's new model sales. New models such as the third-generation Haval H6, the ORA brand and the Tank 300 have received a good market response. New models such as Haval's new flagship SUV concept car HAVALXY, as well as WEY Macchiato and Latte will be launched sequentially in H2. After that, for the ORA Lightning Cat and Punk Cat, will continue to expand the matrix of new energy models. Tank 300 city version, 500, 600, 800 and 700 is expected to be included in the Tank camp successively. As the shortage of chips is alleviating, GWM's sales volume is expected to continue to rise.

On June 28, GWM announced the 2025 Strategy - "Green Smart Play": In 2025, the Company will achieve the global annual sales target of 4 million vehicles, 80% of which are new energy vehicles, with operating revenue exceeding RMB600 billion. In the future, the accumulated R&D investment will reach RMB100 billion. GWM will achieve its first zero-carbon plant by 2023, and ride into top three in global hydrogen energy market share by 2025. We believe that the Company's strategic development objectives for 2025 are clear, and the forward-looking technological innovation layout is expected to continuously strengthen the Company's strength in new energy vehicles and intellectualization in the future, and open up the future valuation space.

Recently, BYD's proposal to spin off its semiconductor business and to list it on the A-share GEM has been accepted, officially opening the way for multiple businesses to obtain value revaluation through the capital market. We believe that with the acceleration of the neutralization strategy, the spin-off listing of other sectors such as blade batteries, commercial vehicles, and photovoltaic energy storage may be successively achieved in the future. The improvement in operational efficiency and value reshaping brought about by the spin-off will push up the Company's potential value. The Company is expected to fully benefit from the dividend of the positive feedback mechanism for capital and company value.

Consumer & Property Management (Timothy Chong)

I have released three update reports covering Semir Garment (002563.HK), LiNing (2331.HK) and Anta Sport (2020.HK) this month. Among them, we highly recommend Anta sport (2020.HK).

Anta Sport announced the company's operating data for Q2 and the 1H on July 8. The company's retail sales value growth in the second quarter was outstanding. Anta's main brand 2Q21 retail sales value increased by 35%-40% Yoy; FILA brand 2Q21 retail sales value Yoy Growth of 30%-35%; 2Q21 retail sales value of other brands increased by 70%-75% Yoy. In the first half of the year, Anta and FILA's retail performance exceeded the company's original expected growth. In addition, the company also announced the `Lead to Win` acceleration plan in the coming 24 months, providing a clear development direction.

The company released the Five-Year Development Strategy and the rapid growth `Lead to Win` in the next 24 months. The strategic goal is divided into two parts, Leader in Scale and High Quality Growth. In the next 5 years, the main brand retail sales value aims to maintain 18-20% CAGR growth, and the market share will increase by 3~5 ppts; in addition, we will strengthen the layout of the first to third-tier cities, and the target will account for more than 50% of salesin the next 5 years, and the number of shopping malls will increase. The online retail sales value will maintain a CAGR growth of 30% in the next 5 years, and its proportion will increase to 40%.

The company Lead to Win is divided into two major directions, eight aspects. The two main directions are rooted in & known for performance sport and brand transformation & growth; in terms of rooted in & known for performance sport, the company proposes three aspects: 1) Continue to sponsor outfits for the national team; 2) Leverage global advanced sports R&D capability; 3) Breakthroughs in core sport categories - running, basketball and women's series. In terms of brand transformation & growth, the company proposes five aspects: 4) Focus on the Summer and Winter Olympics; 5) Win and lead the Generation Z; 6) Speed up DTC transformation and digital transformation; 7) Maintain Anta Kids` position as a market leader 8) Promote sustainable development and sports charities.

TMT (Samuel Sung)

This month I released 2 initial reports of AAC Technologies (2018.HK) and Q Technology (1478.HK). Among them, we highly recommend AAC Technologies.

The gross profit margin of the ACC Technologies's core business dynamic components has risen sharply from 28% in 2020, to 37.4% in the first quarter of 2021 (+11.4 ppts yoy, +9.4% mom). It is expected that the segment's annual gross profit margin will end the three-year continuous downward trend. The company has been deploying on Android customers in recent years, and the revenue and gross profit provided by Android customers to the company will continue to rise in 2020. In the first quarter of 2021, half of the company's segment revenue is contributed by Android customers, and gross profit is approximately 28%. In addition, the company has introduced standardized small-cavity speakers to improve the versatility to be applicable to various Android phone models. Account for about 20%-30% of total shipments in 2021, the company aims to standardize small-cavity speakers to account for about 70%-80% of total shipments in the future. It is expected that the company will still have huge room for growth in the Android market in the future, and its gross profit margin will also increase further.

Until the fourth quarter of 2020, the market share of plastic lenses has steadily increased, and the monthly output of plastic lenses has reached the level of 7kk-8kk per month in the fourth quarter. Its gross profit margin has risen sharply from -2.7% in the second quarter of 2019 to 28% in the fourth quarter of 2020, and its gross profit margin in 2021 reached 36.3%, which is close to the gross profit margin of the leading company Sunny Optical in plastic lenses, mainly due to product quality. In addition, the company's first WLG project has been successfully shipped in the first quarter of 2021, and the first mobile phone equipped with WLG glass-plastic hybrid lens has been promoted in the market. This product uses the 1G5P WLG glass hybrid lens solution. Compared with a plastic lens of the same specification (corresponding to a 6P lens), the light input is increased by 15%, the resolution is increased by 5%, and the overall lens height will be reduced by 5-10%.

From the first quarter report, the revenue is RMB 4.29 billion (+21% yoy). It is expected that the overall revenue will increase in the third and fourth quarters during the peak seasons of mobile phone and other electronic product sales and reverse the company's three consecutive years of declining revenue.

This report is produced and is being distributed in Hong Kong by Phillip Securities Group with the Securities and Futures Commission (“SFC”) licence under Phillip Securities (HK) LTD and/ or Phillip Commodities (HK) LTD (“Phillip”). Information contained herein is based on sources that Phillip believed to be accurate. Phillip does not bear responsibility for any loss occasioned by reliance placed upon the contents hereof. The information is for informative purposes only and is not intended to or create/induce the creation of any binding legal relations. The information provided do not constitute investment advice, solicitation, purchase or sell any investment product(s). Investments are subject to investment risks including possible loss of the principal amount invested. You should refer to your Financial Advisor for investment advice based on your investment experience, financial situation, any of your particular needs and risk preference. For details of different product's risks, please visit the Risk Disclosures Statement on http://www.phillip.com.hk. Phillip (or employees) may have positions/ interests in relevant investment products. Phillip (or one of its affiliates) may from time to time provide services for, or solicit services or other business from, any company mentioned in this report. The above information is owned by Phillip and protected by copyright and intellectual property Laws. It may not be reproduced, distributed or published for any purpose without prior written consent from Phillip.

Top of Page

|

Please contact your account executive or call us now. Research Department Tel : (852) 2277 6846 Fax : (852) 2277 6565 Email : businessenquiry@phillip.com.hk Enquiry & Support Branches The Complaint Procedures |

About Us Phillip Securities Group Join Us Phillip Network Phillip Post Phillip Channel Latest Promotion |

E-Check Login |

Investor Notes Free Subscribe |

|

Contact Us

About Us

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

Phillip Securities Group

Join Us

Phillip Network

Phillip Post

Phillip Channel

Latest Promotion

![]()

![]()

![]()

![]()